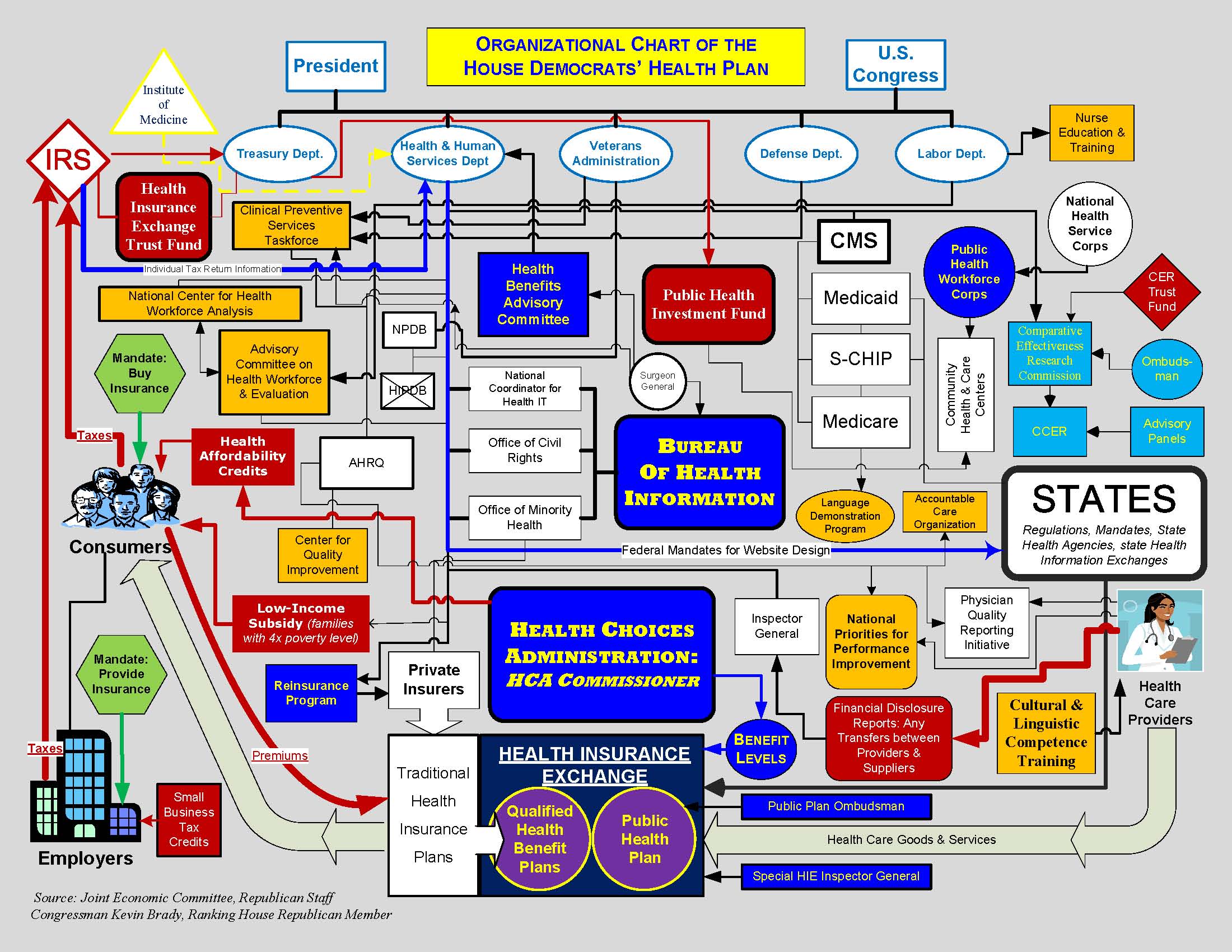

First something new! This will help you to understand how Obamacare has great potential to simplify, improve the system, and reduce costs. Right?

(Click here for larger view)

It didn’t help? Oh, darn!

To a different aspect of this topic: The Chief received flaming replies and was the subject of heartfelt postings (comparing him to Rush Limbaugh!) to his previous posting concerning Obamacare, DEMANDING abject apology on the part of yours truly for having the nerve to question the plans of The One and His Disciples in the Halls of Congress.

Apparently the posting has tripped the trigger over in Madison and has the Madville Times living up to it’s name on this one. Sorry about that Mr. Heidelberger, but can’t we just disagree? No? Oh well…I’m grief stricken. Â If you don’t agree with my conclusions, that’s YOUR business: time will ultimately tell who’s really right on hese, and other issues.

I WILL concede that the below cited provision is not an outright ban on private insurance, but…the devil’s in the details, as is usually the case when dealing with Byzantine proposals for massive new tax-and-entitlement centralized programs, and further apology will be eschewed based on the EFFECT of said program which IMHO results in the eventual end of private insurance. To go back to the piece that originally caught my attention…at risk of possible repetition:

When we first saw the paragraph Tuesday, just after the 1,018-page document was released, we thought we surely must be misreading it. So we sought help from the House Ways and Means Committee. It turns out we were right: The provision would indeed outlaw individual private coverage. Under the Orwellian header of “Protecting The Choice To Keep Current Coverage,” the “Limitation On New Enrollment” section of the bill clearly states: “Except as provided in this paragraph, the individual health insurance issuer offering such coverage does not enroll any individual in such coverage if the first effective date of coverage is on or after the first day” of the year the legislation becomes law.

Based on my understanding of English language, tat seems to be fairly clear.

So we can all keep our coverage, just as promised — with, of course, exceptions: Those who currently have private individual coverage won’t be able to change it. Nor will those who leave a company to work for themselves be free to buy individual plans from private carriers.

If the government gets into the business of offering subsidized health insurance coverage, the private insurance market will wither. Drawn by a public option that will be 30% to 40% cheaper than their current premiums because taxpayers will be funding it, employers will gladly scrap their private plans and go with Washington’s coverage.

Tell me this WON’t happen…if you REALLY believe it won’t, please contact me for some tropical beachfront in NW Moody County, SD – do I have a DEAL for you! So, where does the end of private health programs come in? Attrition, for sure, and small (and large) businesses bailing out of private coverage like mad…let Uncle Sam do it, and figure out the financing too…result, IMHO the attritional death of private coverage. (By the way, this already happened in the UK contributing to the rationing and maltreatment that is far too common over there.)

The nonpartisan Lewin Group estimated in April that 120 million or more Americans could lose their group coverage at work and end up in such a program. That would leave private carriers with 50 million or fewer customers. This could cause the market to, as Lewin Vice President John Sheils put it, “fizzle out altogether.”What wasn’t known until now is that the bill itself will kill the market for private individual coverage by not letting any new policies be written after the public option becomes law.

The legislation is also likely to finish off health savings accounts, a goal that Democrats have had for years. They want to crush that alternative because nothing gives individuals more control over their medical care, and the government less, than HSAs.

The final result will ultimately be the end of private health care and insurance as we know it, not by direct execution, but by an inevitable exercise of a sort of Gresham’s Law applied to health care…bad care drives out good care (unless you are REALLY rich in a way I can’t even begin to imagine, as a semi-retired teacher).

If you, as Mr. Heidelberger is, (and to some extent I also am) are disturbed by the like of the Stanford-MeritCare merger, this too is an inevitable result of the movement towards Obamacare…as these organizations attempt to render themselves “too big to fail” by the standards of even bigger government. (They just want their place at the health care table…no big deal, right, and if Goldman-Sach’s money talks in the halls of Washington, then why not Sanford’s?)

Now, one can decide that this is a positive change in things or not. No problemo, but I continue to call the shots as I see them, whether or not Mr. Heidelberger likes what I say, or agrees with it or whatever…that’s HIS call.

My choice is to reply to specific issues…NOT to get into the gratuitous exchange of invective and personalities in keeping with the counsel of a man much wiser than me: “Never mud-wrestle with a pig. You both get dirty, and the pig enjoys it.”

By the way C.H. – I am honored to be attacked in the same sentence as Rush Limbaugh! It makes me thing I must be doing something RIGHT!